There is something deeply comforting about a fresh, warm cobbler from the oven. An iconic American dessert that reminds us of home. For Russ Goodman and his family, cobbler isn’t just a comfort food; it represents the reward from years of hard work and weathered storms on his farming operation and embodies his passion for serving and promoting the American farmer.

Griffin, GA.: (April 4, 2024): AgSouth Farm Credit Regional Lending Manager Clark David has announced that he is excited to have Thomas James back at AgSouth as a Loan Officer in the Griffin, GA branch office.

Statesville, NC (April 3, 2024) – AgSouth Farm Credit CEO Vance Dalton has announced that the Association’s patronage will be an all-cash distribution of $56 million from AgSouth’s 2023 profits. This distribution will arrive in members’ mailboxes or bank accounts during April.

Fifth-generation farmers Jacob and Emily Nolan operate 1,700 acres of row crops on their family farm in Screven, Georgia. Jacob and Emily established Spring Fever Farms in 2005, building it from the ground up. They have since expanded the operation to include pecans, satsumas, strawberries and other commodities.

The Farm Credit Associations of NC, AgCarolina Farm Credit and AgSouth Farm Credit, announce the fundraising results of $90,000 from the 2023 Pull for Youth sporting clays events. These events benefit NC 4-H and NC FFA. This year marked the seventh annual Pull for Youth event.

The Farm Credit Associations of NC, AgCarolina Farm Credit and AgSouth Farm Credit, announce the 2024 Innovative Young Farmer of the Year and Excellent in Agriculture award recipients. Both award recipients were recognized last month, at the recent NC Tobacco Farm Life Museum, Breakfast with the Commissioner.

Orangeburg, SC.: (February 26, 2024): AgSouth Farm Credit Lending Marketing Manager Will Johnson has announced that he is excited to have Ansley Rast Turnblad as a Marketing Specialist providing marketing support for all of AgSouth’s South Carolina branches.

Vidalia, GA (February 9, 2024): AgSouth Farm Credit Home Loan Origination Manager Michael Hamrick has announced that Rylie Quinn has joined AgSouth Mortgages as the newest Home Loan Officer in the Vidalia, Georgia branch office.

STATESVILLE, NC – AgSouth Farm Credit is proud to have hosted 13 participants in the 2023 AgBiz Program. Many recently attended the AgBiz Conference in Raleigh, NC as the culmination of the program.

Aiken, SC.: (January 23, 2024): AgSouth Farm Credit Regional Lending Manager Troy Brownlee has announced that he is excited to have Helen Schertz at AgSouth as the newest Loan Officer in the Aiken, SC branch office.

Blackshear, GA.: (January 18, 2024): AgSouth Farm Credit Crop Insurance Manager Sandra Meeks has announced that she is excited to have Darcy Davis back at AgSouth as the newest Crop insurance Agent in the Blackshear, GA branch office.

STATESVILLE, NC – Vance C. Dalton, Jr., CEO of AgSouth Farm Credit, announces that AgSouth Farm Credit awarded scholarships for to four students at North Carolina State University, four students at North Carolina A&T University, and five students at the University of Mount Olive for the 2023-2024 academic school year.

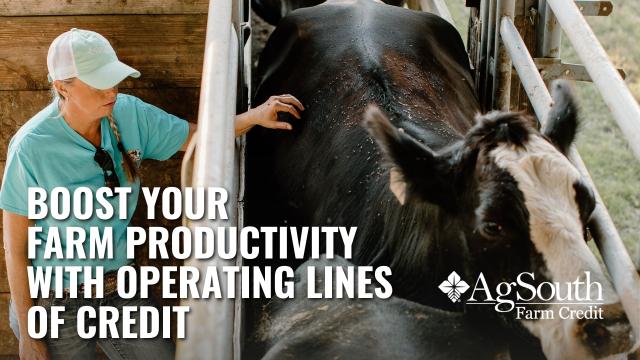

Make a list of essential ways to boost a farm’s productivity, and an operating line of credit will be on it. The benefits are both tangible and intangible, says Stacy Nobles, a relationship lending manager with AgSouth Farm Credit. He and Allen Daley, a relationship lender with AgSouth, have 38 years between them in helping farmers tailor operating lines of credit that best fit their businesses.

STATESVILLE, NC – AgSouth Farm Credit recently awarded grant funding to 42 local non-profit organizations and farmers markets for the 2023-2024 Growing Our Communities Grant program for approximately $200,000. The grant recipients were selected from 276 grant applications received across Georgia, North Carolina, and South Carolina. Each applicant was eligible to receive up to $5,000.

Students from FFA chapters across the state of Georgia had the opportunity to enter and exhibit their wood and metal projects at the Sunbelt Ag Expo in Moultrie, Georgia during the week of October 17-19. The impressive projects are built by middle and high school FFA members and are judged based on quality of work, precision, attention to detail, and difficulty. Projects are divided into four categories: Large Wood, Large Metal, Small Wood, and Small Metal. The Grand Champion and Reserve Champion projects are featured with their winning ribbon throughout the Expo, and students are awarded a cash prize.

You are now leaving our website and being redirected to another site or application. Please be aware that other sites may have their own security and privacy policies, as well as content for which we are not responsible. Thank you.