AgSouth Farm Credit announced today that its Board of Directors has approved a record patronage distribution of approximately $71.2 million to its customers. This marks the largest cash distribution in the Association’s history, representing roughly 70% of AgSouth’s 2025 net income.

Walterboro, SC (March 12, 2026) – AgSouth Farm Credit is excited to announce the grand reopening of its Walterboro branch, located at 529 Bells Highway, following the completion of a full facility rebuild.

Statesville, NC (March 17, 2026) — AgSouth Farm Credit is pleased to announce the appointment of Michael Almond as Executive Vice President – Chief Credit Officer, joining the Association’s Executive Leadership Team. Michael will begin his role on April 1 and will be based in the Statesville Administrative Office.

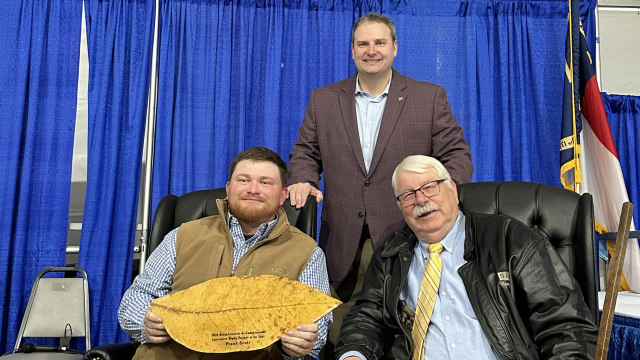

The Farm Credit Associations of NC, AgCarolina Farm Credit and AgSouth Farm Credit, announce the 2024 Innovative Young Farmer of the Year and Excellent in Agriculture award recipients. Both award recipients were recognized last month, at the recent NC Tobacco Farm Life Museum, Breakfast with the Commissioner.

STATESVILLE, NC – The Farm Credit Associations of North Carolina, AgCarolina Farm Credit and AgSouth Farm Credit, proudly recognized the 2026 recipients of the Innovative Young Farmer of the Year Award and the Excellence in Agriculture Award during the 21st Annual Breakfast with the Commissioner, held at the North Carolina State Fairgrounds as part of the Southern Farm Show.

STATESVILLE, NC (February 23, 2026) – AgSouth Farm Credit and AgCarolina Farm Credit are pleased to announce the fundraising results from the 2025 Pull for Youth sporting clays events. These events raised over $90,000 to benefit local NC 4-H and NC FFA chapters. The 2025 event marked the 9th annual Pull for Youth event.

Running a farm means juggling unpredictable weather, rising input costs, shifting markets, and long days. Tax season shouldn’t add more stress to your plate. One of the most effective ways to simplify tax season is to keep accurate records throughout the year.

This month we are partnering with the St. Germain Group to highlight two properties for sale in North Carolina. If you are interested in being featured in our monthly Property Highlight blog, please contact info@agsouthfc.com.

Learn how leasing equipment, facilities, and assets can optimize farm cash flow and support growth as a strategic alternative to traditional financing.

So you want to buy land and build your dream home? There are a couple of different routes you can take in making this dream a reality. You can buy the land now and wait to build, or you can buy the land and build the home at the same time. Both routes have benefits.

Buying an existing country home with acreage? Learn what to know before you buy, from rural living considerations to financing and appraisal requirements.

Learn how to read and build a farm income statement by understanding income, expenses, gross margin, fixed costs, and net farm income to measure profitability.

This month we are partnering with Crosby Land Company to highlight four properties for sale in Georgia. If you are interested in being featured in our monthly Property Highlight blog, please contact info@agsouthfc.com.

In the heart of Ridge Spring, South Carolina where the soil is rich and the community even richer, Yon Family Farms stretches across hundreds of acres of pasture, promise, and pecan trees. More than a cattle operation, more than a business, it’s a family legacy, a living example of what can grow when faith, hard work, and love of the land come together.

In deep South Georgia, the Sanders Honey Company has been crafting more than just honey - they’ve been nurturing a legacy. What began as a modest family endeavor has blossomed into a beloved community cornerstone, where every jar tells a story of hard work, determined drive, and desire for community.